HDB Financial Services ₹12,500 Crore IPO Launch in June 2025: Price Band, Dates & Valuation at ₹62,000 Crore

HDB Financial Services IPO Summary

Mark your calendars! In one of the most anticipated financial events of 2025, HDB Financial Services Ltd., a subsidiary of HDFC Bank, is preparing to roll out its ₹12,500 crore initial public offering (IPO) by the end of June. The issue is a combination of fresh issue of 3.38 crore shares aggregating to ₹2,500.00 crores and offer for sale of 13.51 crore shares aggregating to ₹10,000.00 crores. This offering is poised to become India’s biggest-ever IPO by a Non-Banking Financial Company (NBFC) and among the largest in the overall market for the current calendar year—surpassed only by Hyundai Motor India’s ₹27,000 crore issue last year.

The HDB Financial Services Ltd. IPO window for public subscription is expected to open between Wednesday June 25 and Friday June 27, 2025, Looking to Invest Early. The anchor investor portion slated for Tuesday June 24. The allotment for the HDB Financial IPO is expected to be finalized on Monday, June 30, 2025. HDB Financial IPO will be list on BSE, NSE with a tentative listing date fixed as Wednesday, July 2, 2025. The IPO will be offered at a price band of ₹700–₹740 per share, and investors can place bids for a minimum lot size of 20 shares or multiples thereof. The minimum amount of investment required by retail investors is ₹14,000. But it is suggested to the investor to bid at the cutoff price to avoid the oversubscription senerio, which is about to ₹14,800. The minimum lot size investment for sNII is 14 lots (280 shares), amounting to ₹2,07,200, and for bNII, it is 68 lots (1,360 shares), amounting to ₹10,06,400. If successful at the upper end of the price band, HDB Financial Services will attain a post-money valuation of approximately ₹62,000 crore ($7.2 billion).

Also Read: Why Health Insurance is Important for Your Financial Future

HDB Financial Services IPO Details at a Glance

| IPO Open Date: | June 25, 2025 |

| IPO Close Date: | June 27, 2025 |

| Face Value: | ₹10 Per Equity Share |

| IPO Price Band: | ₹700 to ₹740 Per Share |

| Issue Size: | Approx 12,500 Crores |

| Fresh Issue: | Approx ₹2,500 Crores |

| Offer for Sale: | Approx 13,51,35,135 Equity Shares |

| Issue Type: | Book Built Issue |

| IPO Listing: | BSE & NSE |

| Retail Quota: | Not more than 35% |

| QIB Quota: | Not more than 50% |

| NII Quota: | Not more than 15% |

| DRHP Draft Prospectus: | Click Here |

| RHP Draft Prospectus: | Click Here |

| Anchor Investors List: | Click Here |

IPO Distribution and Structure

The HDB Financial Services IPO consists of:

- Fresh issue: ₹2,500 crore

- Offer for sale (OFS) by parent HDFC Bank: ₹10,000 crore

- Total issue size: ₹12,500 crore

- Price Band: ₹700–740 per equity share

- Minimum Lot Size: 20 shares and multiples thereafter

- Listing Exchanges: BSE and NSE

- Tentative Listing Date: July 2, 2025

- Up to 50% of the shares will be allocated to Qualified Institutional Buyers (QIBs). These are institutional investors such as banks, mutual funds, and insurance companies.

- A minimum of 15% of the shares will be reserved for Non-Institutional Investors (NII). These typically include high-net-worth individuals (HNIs) or corporate bodies investing more than ₹2 lakh.

- At least 35% of the offering will be available for retail investors. These are individual investors applying for shares with a total value of less than ₹2 lakh.

Parent company HDFC Bank, which holds a 94.3% stake in HDB Financial Services, is divesting a portion through the OFS. Proceeds from the fresh issue will be used for the augmentation of Tier-1 capital to support future growth, including onward lending and capital adequacy compliance.

HDB Financial Services GMP, Grey Market Premium 2022

HDB Financial Services GMP as of 23rd Jun 2025 is 46. Stay tuned for the latest IPO GMP numbers of HDB Financial Services.

| HDB Financial Services GMP Date | GMP | IPO Price | Expected Listing Gain |

| GMP is as on 19 Jun 2025. | 93 | 740.00 | 833 (13%) |

| GMP is as on 20 Jun 2025. | 75 | 740.00 | 815 (10%) |

| GMP is as on 23 Jun 2025. | 90 | 740.00 | 830 (12%) |

| GMP is as on 23 Jun 2025. | 46 | 740.00 | 786 (7%) |

| GMP is as on 24 Jun 2025. | 70 | 740.00 | 810 (9%) |

| GMP is as on 25 Jun 2025. | 74 | 740.00 | 814 (10%) |

| GMP is as on 26 Jun 2025. | 50 | 740.00 | 790 (7%) |

| GMP is as on 27 Jun 2025. | 52 | 740.00 | 792 (7%) |

| GMP is as on 28 Jun 2025. | 57 | 740.00 | 797 (8%) |

| GMP is as on 30 Jun 2025. | 58 | 740.00 | 798 (8%) |

| GMP is as on 01 Jul 2025. | – |

Regulatory & Strategic Imperatives

The IPO is not merely a strategic move but also a regulatory requirement. Under the Reserve Bank of India’s (RBI) October 2022 circular, NBFCs classified as “Upper Layer” must compulsorily list their shares within three years of classification. HDB Financial was notified under this classification in September 2022, making a listing deadline of September 2025 imperative.

The company’s board had already granted in-principal approval for the IPO on July 20, 2024, and a committee of directors was formed to execute the listing process. The Draft Red Herring Prospectus (DRHP) was filed in October 2024, and an Updated DRHP (UDRHP) has recently been submitted as part of the final compliance stage before the Red Herring Prospectus (RHP) filing.

Also Read: How to Make Side Hustles and Stand in Market in 2025-26

About HDB Financial Services: India’s biggest-ever (NBFC).

Established in 2007 and headquartered in Mumbai, HDB Financial Services Ltd. is a leading NBFC in India, focusing on retail and SME lending, loan servicing, and insurance services.

Key operational highlights:

- Enterprise Lending – working capital, business expansion, equipment finance

- Asset Finance – vehicle loans, commercial equipment loans

- Consumer Finance – personal loans, consumer durable loans, gold loans

- Branch Network: 1,680+ branches across India

- Focus Areas: Retail loans, SME loans, vehicle finance, loans against property (LAP)

- Customer Base: Several million across Tier-1 to Tier-4 cities

- AUM Mix: Diversified portfolio with strong retail and small-business focus

- Employee Strength: Over 25,000 professionals

Promoter: HDFC Bank Limited

Incorporation Date: June 4, 2007

Registered Office: Ahmedabad, Gujarat

Corporate Office: Mumbai, Maharashtra

Market and Stakeholder Sentiment

The market response to HDB Financial’s IPO is being closely watched due to its magnitude and HDFC Bank’s involvement. If the issue is fully subscribed and priced at the upper band, it would mark one of the most successful NBFC listings in Indian financial history.

According to insiders, investor sentiment remains upbeat, driven by:

- The strong pedigree of HDFC Bank

- HDB’s consistent growth and earnings profile

- Favorable market conditions

- A robust retail and SME loan book

Shares of HDFC Bank (NSE: HDFCBANK), the parent company, closed at ₹1,933.10 on Thursday, reflecting marginal change amidst the IPO anticipation.

Click Here to Start Investing

4. Financial Performance Overview

A. Key Financial Metrics (₹ in billion):

| Parameter | FY22 | FY23 | FY24 |

| Total AUM | 614.4 | 700.8 | 902.3 |

| PAT | ₹10.2 bn | ₹17.8 bn | ₹24.6 bn |

| Net Worth | ₹79.6 bn | ₹103.1 bn | ₹127.8 bn |

| Gross Loan Book | ₹853.8 bn | ₹930.5 bn | ₹986.2 bn |

| GNPA | 4.97% (FY22) | 3.73% (FY23) | 2.66% (H1 FY25) |

| NNPA | 2.39% (FY22) | 1.55% (FY23) | 1.03% (H1 FY25) |

CAGR (FY22–FY24):

- AUM Growth: 21.18%

- PAT Growth: 55.98%

These figures illustrate robust profitability, strong asset quality improvements, and prudent risk management, especially significant in a volatile NBFC market.

IPO Book Running Lead Managers (BRLMs)

HDB Financial’s IPO syndicate is backed by an impressive line-up of 12 investment banks, underscoring the scale and importance of the issue:

- JM Financial

- BNP Paribas

- BofA Securities

- Goldman Sachs (India) Securities

- Jefferies India

- HSBC Securities & Capital Markets

- IIFL Capital Services

- Morgan Stanley India

- Motilal Oswal Investment Advisors

- Nomura Financial Advisory

- Nuvama Wealth Management

- UBS Securities India

The legal counsel for the issue is Cyril Amarchand Mangaldas, and the registrar is MUFG Intime India (Link Intime).

Use of IPO Proceeds

Only the ₹2,500 crore from the fresh issue will go to the company. As stated in the DRHP:

- Primary Purpose: Augmenting Tier-I Capital to support:

- Future business growth

- Onward lending

- Strengthening regulatory capital ratios

- Other Uses: Covering offer-related expenses

- Deployment Period: FY25 and FY26

No proceeds from the OFS portion will be retained by the company; they will be received by HDFC Bank.

Industry Context and Competitive Landscape

According to CRISIL:

- NBFC credit grew at a CAGR of 11% (FY19–FY24) and is projected to rise by 15–17% (FY24–FY27)

- Key NBFC peers: Bajaj Finance, Cholamandalam, Shriram Finance, Tata Capital, etc.

- HDBFS holds a strategic mid-tier position—a fast-growing player with improving asset quality

Market Differentiators:

- HDFC Bank’s backing

- Diversified lending model

- Extensive BPO and collections backbone

Strengths of HDB Financial Services

- Strong Parentage: Backed by HDFC Bank

- Diversified Product Base: Presence in retail, MSME, asset finance

- Consistent Profitability: Demonstrated through rising PAT and low NPA levels

- Operational Efficiency: Integration of BPO with lending gives cost and control advantages

- Robust Risk Framework: Strong underwriting, improved GNPA/NNPA ratios

Risks and Challenges

- Concentration Risk: High reliance on India-only market

- Regulatory Compliance: RBI compliance for NBFC-ULs is stringent

- Credit Risk: Exposure to SME and vehicle finance sectors prone to economic cycles

- Operational Complexity: Managing collections, especially in semi-urban regions

- Digital Competition: Rising fintech NBFCs may challenge traditional models

Growth Opportunities

HDBFS is well-positioned to capitalize on:

- MSME Credit Boom: Formalization of small businesses boosts loan demand

- Vehicle and Equipment Financing: Infrastructure growth = higher demand

- Tech Integration: More efficient underwriting, analytics, credit scoring

- Cross-Selling: Leveraging HDFC ecosystem (insurance, mutual funds)

- Urban-Rural Bridging: Expanding semi-urban presence

Shareholding and Post-IPO Structure

| Category | Pre-IPO Shareholding | Post-IPO Holding (approx.) |

| HDFC Bank | 94.36% | Expected to reduce significantly |

| Public | 0% | Expected to rise to 20%+ depending on final allotment |

| Employees & HDFC Shareholders | Reserved quota applicable |

Conclusion: A Landmark NBFC IPO

The HDB Financial Services IPO is a significant milestone in India’s capital markets. It marks a rare opportunity to invest in a retail-focused, high-growth NBFC with established governance, parent support from HDFC Bank, and demonstrated profitability.

With a strong foothold in consumer and SME lending, improving credit quality, and a commitment to growth through capital augmentation, HDBFS is likely to attract wide investor interest.

As it heads toward public listing, investors and analysts alike will be watching closely to see how the company delivers on its promise of growth, stability, and returns—hallmarks of a well-run NBFC in India’s evolving credit landscape.

Investors eyeing quality exposure in the NBFC space should closely track this issue as the June 25 opening date approaches.

Also Read: How to Build Passive Income for Long Run in 2025-26

HDB Financial Services Ltd.’s Pros & Cons

1. Pros

- HDB Financial Services claims to have served 17.5 million customers as of September 30, 2024, with customer growth at a compound annual growth rate (CAGR) of 28.22 percent since FY22.

- The company claims to focus on underbanked and ‘new to credit’ segments, with customers classified as ‘new to credit’ accounting for 12.02 percent of the total gross loan book, as of September 30, 2024. The company further states that its top 20 customers contribute less than 0.36 percent of total loans, reflecting a de-risked and low-concentration lending profile.

- The company claims to offer 13 distinct lending products across enterprise lending, asset finance, and consumer finance, each with independent operations and dedicated management teams. Its loan portfolio is reportedly balanced, with no single product exceeding 25 percent of the total gross loan book. HDB also claims that its portfolio has remained resilient across multiple economic disruptions, including the 2008 financial crisis, the 2018 NBFC liquidity crunch, and the COVID-19 pandemic.

- HDB Financial Services claims to operate a pan-India ‘phygital’ distribution model comprising 1,772 branches across over 1,162 towns and cities, with more than 70% of branches located in tier 4+ towns. The company claims its internal sales force is supported by a large external distribution network of over 140,000 retailers and dealer touchpoints, along with partnerships with 80+ brands and original equipment manufacturers (OEMs). Additionally, HDB claims to enhance reach through digital platforms such as its own mobile application and fintech partnerships.

- The company claims to maintain a dedicated in-house underwriting team of around 4,500 professionals and a collections workforce of over 12,000. It reportedly uses a hybrid credit model combining centralised and decentralised underwriting, along with data-driven decision systems and customised scorecards for high-precision risk assessment. HDB further claims that over 95% of its loans and collections, as of the period ended September 30, 2024, are processed through digital or banking channels, and that its low gross non-performing assets (GNPA) (1.90%) and net non-performing assets (NNPA) (0.63%), as of FY24, reflect the strength of its credit and collections framework.

- HDB Financial Services claims to have built an advanced and scalable digital infrastructure spanning sourcing, onboarding, underwriting, servicing, and collections. It has developed paperless onboarding journeys, artificial intelligence/machine learning (AI/ML)-driven credit scorecards, and application programming interface (API) integrated tools for employees and partners. Its ‘HDB On-the-Go’ mobile application enables customers to avail loans, track applications, access documentation, and raise service requests.

- The company claims to have access to one of the most cost-effective and diversified borrowing bases among Indian NBFCs, supported by a CRISIL and CARE credit rating of AAA (Stable), the highest rating in the sector.

- The company claims to have a high debt-to-equity ratio of 5.93x as of September 30, 2024, contributing to a strong return on average equity of 16.39 percent.

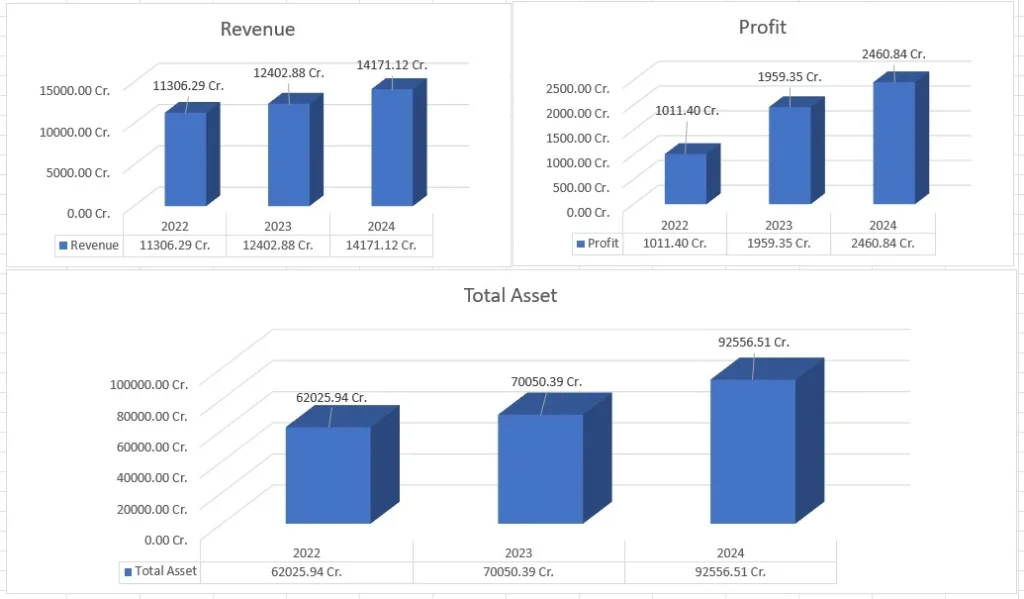

- The company has witnessed a consistent increase in revenue from operations and profit after tax (PAT). Revenue from operations increased from Rs 11,306.29 crore in FY22 to Rs 12,402.88 crore in FY23 and Rs 14,171.12 crore in FY24. PAT increased from Rs 1,011.4 crore in FY22 to Rs 1,959.35 crore in FY23 and Rs 2,460.84 crore in FY24.

2. Cons

- Unsecured loans accounted for Rs 28,517.36 crore (28.92 percent) of the company’s total gross loan book in the period ended September 30, 2024, Rs 25,858.95 crore (28.66 percent) in FY24, Rs 18,998.83 crore (27.13 percent) in FY23, and Rs 16,200.4 crore (26.42 percent) in FY22. Any adverse change in customer repayment behaviour or economic distress could severely impact recoverability, as these loans are not backed by collateral. The company may be forced to increase its provisions for credit losses, which would negatively affect earnings.

- Secured loans accounted for Rs 70,106.85 crore (71.08 percent) of the company’s total gross loan book in the period ended September 30, 2024, Rs 64,358.98 crore (71.34 percent) in FY24, Rs 51,031.87 crore (72.87 percent) in FY23, and Rs 45,125.93 crore (73.58 percent) in FY22. Any decline in collateral value, especially for depreciating assets like automobiles, or delays in enforcement proceedings may negatively impact the company’s ability to recover dues and affect its overall financial condition.

- As a non-deposit taking NBFC that relies on wholesale borrowings, HDB Financial Services is exposed to fluctuations in interest rates, which directly affect its finance costs. In FY24, while net interest income increased to Rs 6,292.4 crore from Rs 5,415.86 crore in FY23, the net interest margin declined to 7.85 percent from 8.25 percent, during the same period, due to rising borrowing costs. Any mismatch in the repricing of assets and liabilities, particularly in periods of rate volatility, could adversely impact the company’s profitability, cash flows, and overall financial condition.

- The company’s business is impacted by seasonality, with higher demand for consumer finance products during festive months and increased demand for asset finance products in the fourth quarter of the fiscal year. Any inability to effectively manage this fluctuation in demand could adversely affect its business and financial condition.

- The company, its promoter, and directors are involved in certain legal proceedings, including criminal and tax-related matters. Any adverse judgments in any of these cases could be detrimental to the company’s business prospects.

- The company reported negative cash flow from operating activities amounting to Rs 9,208.85 crore in the period ended September 30, 2024, Rs 16,736.04 crore in FY24, and Rs 6,850.61 crore in FY23. Additionally, negative cash flow from investing activities amounted to Rs 2,145.56 crore in FY24 and Rs 703.28 crore in FY22. The company also reported negative cash flow from financing activities in FY22, amounting to Rs 1,499.54 crore. Furthermore, the company experienced a net decrease in cash and cash equivalents amounting to Rs 81.3 crore in FY23 and Rs 215.72 crore in FY22. If cash outflows continue to exceed inflows in the future, the company may face liquidity challenges.

- As of September 30, 2024, the company had contingent liabilities amounting to Rs 613.72 crore. If any of these contingent liabilities materialise, it may adversely affect the company’s financial condition. As of September 30, 2024, the company had outstanding financial indebtedness of Rs 82,681.1 crore. Any failure to service or repay these loans can hurt the company’s operations and financial position.

Overall, HDB Financial Services IPO presents an opportunity for investors to participate in the growth of the Indian Financial market. However, it is important to weigh the risks and consider the company’s financial performance and competitive landscape before making an investment decision.

Frequently Asked Questions

Q. What is the Bidding Start date of HDB Financial Services?

A. HDB Financial Services Ltd Bidding Start date is Wednesday, June 25th 2025.

Q. What is the Bidding End date of HDB Financial Services?

A. HDB Financial Services Ltd Bidding End date is Friday, June 27th 2025.

Q. What is the price band of HDB Financial Services?

A. HDB Financial Services Ltd Price band is set to 700 to 740 per equity shares.

Q. What is the Lot Size of HDB Financial Services?

A. HDB Financial Services’s Lot Size is 20 Shares and multiple of 20 shares thereafter.

Q. What is the Share allotment date of HDB Financial Services?

A. HDB Financial Services’s Shares allotment date is Monday, June 30, 2025.

Q. What is the Share credit date in Demat of HDB Financial Services?

A. HDB Financial Services’s Shares credit date in Demat is Monday, June 30, 2025.

Q. What is the Listing date of HDB Financial Services?

A. HDB Financial Services’s Listing date is Wednesday, July 2 2025.

Disclaimer

The information provided in this article about the HDB Financial Services is for informational purposes only and does not constitute financial advice. Finance Gurukul does not recommend investing in any specific securities or investment strategies. It is important to conduct your own research and due diligence, and to consult with a qualified financial advisor before making any investment decisions.

Investing in the stock market involves inherent risks, and investors may lose some or all of their invested capital. Past performance is not necessarily indicative of future results.